![[later] I don't get why our pizza slices have such terrible reviews; the geotextile-infused sauce gives the toppings incredible slope stability!](https://imgs.xkcd.com/comics/tariffs.png "[later] I don't get why our pizza slices have such terrible reviews; the geotextile-infused sauce gives the toppings incredible slope stability!")

1) You want a pizza made from another region.

2) However, you must sell them some your ingredients before it can be made.

3) They charge a “tariff” to protect the income of their local farmer’s for other ingredients. You’re willing to pay the “tariff” because you like your ingredients better.

4) The pizza maker sells you the final pizza with a standard sales tax but no tariff

5) You paid the higher price and they made money from the tariff.

Trump is charging tariffs to increase the costs from other regions for several reasons. A) To negotiate down tariffs from other regions. B) Lower tariffs mean you pay a lower cost for your special pizza. C) To whittle down our regions deficit. D) and/or To increase local “ingredients” growth at lower cost for you.

Recently, noted VC Marc Andreessen kicked off a discussion about debanking, in a podcast with his co-founder Ben Horowitz (begins at 7:42) and in an appearance on Joe Rogan’s podcast). The venture firm they founded, a16z, also published a brief on this topic.

The central thrust, quoting a16z’s brief (ellipsis in original): “Debanking can therefore be used as a tool or weapon systemically wielded by specific political actors / agencies against private individuals or industries without due process. Imagine if the government decided who could or couldn’t get electricity merely because of their politics, or some arbitrary reason… without having to explain, notify, or offer recourse. That’s what’s happening with debanking.”

If you are new here, you are presently reading a column which routinely covers compliance-oriented topics at the intersection of the financial system and technology companies. This topic is pretty central to my beat, and I have some relevant personal knowledge.

“It’s not a conspiracy theory if people really are out to get you.” sums up part of my reaction to this, but only part. There exists some amount of conflation between what private actors are doing, what state actors have de facto or de jure commanded that they do, and which particular state and political actors have their fingers on the keyboard. These create a complex system; the threads are not entirely divorced from each other.

A few disclaimers:

I previously worked for Stripe, and am currently an advisor there. Stripe is not a bank, but many regulated financial institutions have similar considerations. I’m not speaking for them. Stripe does not necessarily endorse things I say in my own spaces.

The recent debanking discourse focuses (and overfocuses; see below) on crypto. I am (somewhat notoriously) a crypto skeptic. Arguments aren’t soldiers; the truth is the truth. The truth sometimes favors crypto advocates in this discussion, and where it does, I will cite sources extensively. Where it doesn’t, I will mostly cite sources extensively.

The debanking discussion arises from an explicitly political project. Moreover, questions of public policy are frequently political in a democracy. The ballot box is the ultimate check on government abuse of power. While I have no project here, and try to be non-partisan in professional spaces, to ease the fears of crypto fans: I’m definitely not a secret Warrenite.

Closing bank accounts

“Debanking” describes a cluster of behaviors.

The most salient one is involuntarily closing a customer’s bank account, often a long-established one, optionally without presenting a reason. Because “debanking” is an advocacy term, that often gets conflated with declining to open an account for a person or a business.

These two things are very different in their impact on the person/firm and in our moral intuitions. It’s the difference between getting divorced and being turned down for a date.

Advocates often invoke a user-centric perspective of debanking, focusing on the impact on individuals/firms. Then, they conflate it with regulators’ decisions regarding bank supervision, in ways which are facially not about direct user impact. We will return to bank supervision later.

Industry doesn’t call it “debanking.” This is partly for the usual corporate euphemism reasons. This is partly because industry does not always share assumptions of how the world should work with advocates, and is concerned that “debanking” smuggles in those assumptions.

So when one discusses this with colleagues, one might use words like offboarding, derisking, closing the accounts of a customer, etc.

There is often an implication, and much rarer a reality, that the debanking decision is not one of a single financial institution. Sufficiently correlated “independent” decisions by financial institutions could deprive a firm or individual of access to banking services. We will explore some coordination mechanisms, which are overstated, and some correlation mechanisms, which are poorly understood.

We’re hearing about debanking because it sometimes affects socially established wealthy entrepreneurs and their companies. Some people it happened to are densely networked and also affiliated with talented communicators that have (in the parlance of our times) a platform. It is important to say from the jump that this is not the typical profile.

A huge majority of all people who find their accounts involuntarily closed will have been let go for credit risk or operational cost reasons. Overdraft your account repeatedly and look unlikely to be able to pay the fee for this service? Expect to lose that account, and probably all other accounts at that institution.

Do you know anyone with a parent advanced in years, who is dealing with challenges of aging, perhaps has gotten scammed a time or three, and might occasionally lash out at customer service employees? Debanking is more relevant to their interests than they might currently appreciate.

Decisions to debank an individual will often debank their controlled entities, and vice versa. Debanking will also not infrequently swiftly cascade to accounts in the same household, regardless of title (non-specialists can round this to “name on the account”; industry can’t). Banks institutionally consider those accounts in the same household to be highly likely to be under common control, regardless of what paperwork, account holders, or politically influential subcultures believe. This is an area in which the mores of the banking industry are much closer to the traditional middle class than to coastal elites.

Sometimes, though, one gets one’s accounts closed because one has activities which are outside a bank’s risk tolerance or contrary to their compliance posture. This was cited to me both times I was debanked.

Two debanking anecdotes explained

Once upon a time, I had a U.S. checking account. One day, the bank called me, and asked me why I was averaging two incoming ACH transfers a day. I told them that I ran a sole proprietorship selling software over the Internet. The ACH transfers were from from my two payment providers, which paid me out my sales (less fees) once per business day. The bank thanked me for my explanation and told me they thought the business sounded legitimate. Then they said I had 30 days to move the business’ funds flow to a different bank, or they would close all my accounts.

“Banksplain that offboarding?” Typical retail consumer checking accounts are, on the spectrum of the full menu of banking services, extremely low-risk, not a focus of bank examiner time, and institutionally preferred by both banks and regulators because of core financial access concerns. Accordingly, the amount and degree of monitoring a bank invests in the consumer checking line of business will be relatively low, in line with a risk analysis it performed. Its regulator has read that analysis and decision, and expressed no objection to it.

This particular bank did not, at the time, have a small business practice within its personal banking division. Very many banks do, but this particular bank did not. And thus this bank had not built out the higher degree of policies and procedures that would support small business banking. A surprising example of a small business that demands drastically more thought than you would think is discussed in detail below. The bank, on learning I had a sole proprietorship banked with them, considered that behavior innocent but not supportable, not because it didn't like my business but because it knew it had no built out infrastructure to support any business.

At the second institution, I once checked my U.S.-organized individual retirement account from a Japanese IP address. I had done that many times, but I did it one last time, too. This caused a short phone call, where the bank’s affiliate confirmed that I indeed lived in Japan, then informed me the account would be immediately restricted and then closed. I would need to make arrangements to request my shares be transferred to a new (U.S.) brokerage account, or authorize them to sell and mail me a check.

“Banksplain that offboarding?” This was likely downstream of a procedure implemented to ensure that the institution’s affiliated securities firm did not act outside the scope of its broker-dealer licenses, which (the institution was aware) did not include any with Japanese regulators.

When these events happened, it was very annoying. I did not contemporaneously understand why they were happening. They required me to take time away from life, my day job, and business to make more phone calls, learn more things about the financial industry, and ultimately open new accounts.

That is the typical end to a debanking story. “And then, I opened a new account.”

Immigrant communities keep lists of which banks most want their business. So does the community of people who run small software businesses online. And so, while immigrants and small software companies deal with substantially more banking friction than the typical American working for Google or a university does, they are both very bankable.

Consider crypto entrepreneurs who have received an offer of investment of several million dollars. One might be able to hold the ideas in one mind simultaneously that a) there is some diversity of life experiences in that group but b) on average though, they are very socially advantaged, when considered on most of the usual axes. Despite those substantial advantages, it has been persuasively alleged that their companies and the entrepreneurs themselves routinely suffer debanking.

I also understand this to be true, in large part downstream of one risk factor that they hit more than almost all legal businesses of comparable scale and sophistication. There have been times and places where this challenge made crypto firms almost unbankable to the extent banks knew what they were doing. And it directly drives decisions against crypto founders and employees.

Debanking specifically for AML risk

I’ve written extensively about KYC and AML and will not recap all of it here. Banks have a panoply of obligations under regulation. One of those is that they have to write AML policies, including policies which identify high-risk activities. Then they have to follow those policies. You can overpromise but you cannot underdeliver; after you’ve told a regulator you will do X, not doing X can result in fines and other punishments, even if the regulator did not tell you to do (specifically) X.

Before we reach crypto, consider AML risk and its consequences among money services businesses.

Running a money services business (MSB) is virtually universally called out as a high-risk activity by banks’ internal AML policies. Explaining why would require explaining the entire history and object of AML. Please just take as writ for the moment: all banks have a list, those lists rhyme with some variation, and MSBs are on all the lists.

Some banks have built out so-called enhanced due diligence (EDD) programs under which they will bank MSBs. Many banks have not; if a business banking at one identifies itself as an MSB, or if their ongoing monitoring of transactions suggests one is probably an MSB (for example, if there are ACH pull from Western Union for tens of thousands of dollars, which will suggest to an analyst that the business is probably a Western Union agent transaction above the de minimis threshold), the bank intends that business to get a letter.

Whether they successfully execute on the letter, and the decision the letter announces, varies, but in terms of intent, they intend to consistently reach the decision given similar facts.

That letter will, in all likelihood, not be candid as to what is happening or why. It may not cite that the customer is an MSB. It may not cite why the bank believes that. It will not recount the bank’s internal AML policies which identify being an MSB as a high-risk activity, though it might say four or five templated words about risk. It will not explain the bank’s strategic decision to not invest in a compliant EDD program that would allow it to service MSBs.

No, the letter will say that the bank is closing the customer's accounts.

It may describe this as a "business decision", using those two words, of the bank. It will often say that this decision is final. The decision is probably not actually final. That is an opening negotiating position, like “We don’t negotiate salaries.” If you don’t argue the point, it has achieved its objective. The grain of truth within it is “We probabilistically think that talking with the typical recipient of this letter is negative expected value.”

Why doesn’t the bank want to talk with the typical recipient about it? Because the typical MSB is a bodega with a sideline in alternative financial services.

You might think that it is absurd that the government would concern itself with MSBs that are clearly the sideline of the local bodega. Without reaching the question of whether this priority is absurd, I invite you to peruse the Financial Crime Enforcement Network’s Enforcement Actions For Failure To Register As A Money Services Business. These are a small sample of real enforcement actions. That sample was chosen by FINCEN and I think reasonable people understand it was not chosen by FINCEN with a goal of embarrassing FINCEN or the entire AML regime that ensures FINCEN employees will have a job tomorrow.

I will take the liberty of fictionalizing names here, to give you the flavor of real people with real businesses that FINCEN both a) prosecuted and b) posted trophies of pour encourager les autres : Bob Smith d/b/a Bob’s Fast Gas. Taro’s Snack Shop, Inc. Cheap Phonez 4 U, Inc. Ben Goldberg d/b/a Kosher Foods.

FINCEN has posted the full text of each settlement, frequently including a restatement of their alleged violations. In many of those documents (not all of them!), if one credits FINCEN’s narrative as Gospel truth, one will believe: yeah, this is absolutely a bodega. The Financial Crimes Enforcement Network has jammed up the guy behind the counter because he failed to have a written AML/KYC policy and because when he traveled overseas the person he hired to mind the store was not trained in AML. Having won the case, they fined him $10,000. Given that, a fair-minded reader immediately assumes the bodega is probably not actually a front for the Colombian drug cartels, Hamas, or a foreign intelligence operation.

With this well-evidenced understanding of FINCEN’s… quixotic interest in the crime of selling money orders and also laundry detergent and delicious sandwiches, you can understand why a bank, attentive to FINCEN’s desires here, is doing something that strikes many people as insane. It has employed teams of people whose job is to make sure it sifts the rogue bodegas from the garden-variety bodegas before FINCEN asks “Why did you move money for a rogue bodega!? How many times do we have to tell you people! BE ON THE LOOKOUT FOR ROGUE BODEGAS.”

Running EDD processes and ongoing monitoring is expensive. Banking a bodega isn’t very lucrative. And thus most banks won’t bank a bodega that is also an MSB, despite them having no particular malice against bodegas or the people who run them. This won’t change if the bodega owner calls to them to protest that he is a legitimate businessman, that this debanking is un-American, or that he feels like they are discriminating against him for being an immigrant. That’s a conversation the bank has had a thousand times and never want to have again… with a bodega owner.

Some MSBs are fintechs. They have teams of people who are extremely aware of financial regulation. Those professionals intentionally chose a bank which was capable of banking at least some MSBs. They then had a laborious bespoke conversation about risk tolerance and mutually agreed-upon compliance procedures.

More than zero fintechs have been debanked over the years, but they probably don’t first learn about it from a paper letter. Their team of people who do bank things all day would have heard from the team of people that do fintech things all day, likely beginning many moons ago. And if they got the letter, they would understand generally why they got the letter, and not be so oblivious as to trust the literal text of the letter.

Class is an interconnected set of culture, scripted behaviors, and the advantages and disadvantages that attach to them. The culture that is the American professional-managerial class has a relationship with truth which occasionally confounds outsiders to it. An American PMC member, particularly one with a professional specialization in banking, understands an offboarding letter to be a ritual object rather than something meant to be taken literally.

Many regular people who get the offboarding letter are confused and upset. Most people who get this letter are insufficiently expert in the financial system to understand what is going on. Many of them are (perhaps sensibly) enraged that the bank seems reluctant to offer answers. If they successfully pry answers out of the bank, the answers sound like nonsense or change constantly.

Here, advocates often say that banks lack fundamental humanity, regard for their customers, or simple competence. I’d tell them that is neither here nor there, but the challenges described in Seeing like a Bank drive far more of this than malice, apathy, or incompetence as such. It is a systems issue.

But AML-driven offboarding has one particular spectral signature which is worse than normal debanking, which will always be a confusing, unpleasant experience for most customers.

Some of these customers are getting the letter because the bank looked into their account after a transaction was flagged as suspicious. This generally happens because an automated system twinged on it. Most of the so-called “alerts” are false positives, but banks are required to have and follow a procedure to triage them. That procedure is typically “Send a tweet-length summary of the alert to an analyst and have them eyeball things.” Every bank needs at least one person triaging alerts; the largest banks have thousands.

What if the analyst, on the basis of their training, experience, and data available from the alert system and from the account history they can access, decides that a transaction has… more than nothing irregular about it? Then they compose a specially formatted memo.

That memo is called a Suspicious Activity Report (SAR). The bank files it with FINCEN, via a computer talking to a computer after the analyst pushes some buttons. Then the analyst goes back to triaging incoming alerts.

Busting bodegas is a sideline for FINCEN; receiving SARs is their main job.

A SAR is not a conviction of a crime. It isn’t even an accusation of a crime. It is an interoffice memo documenting an irregularity, about 2-3 pages long. Banks file about 4 million per year. (There are some non-bank businesses also obliged to file them, but nobody is presently complaining about decasinoing, so ignore that detail. Banks are the central filers of SARs.) For flavor: about 10% are in the bucket Transaction With No Apparent Economic, Business, or Lawful Purpose. FINCEN has ~300 employees and so cannot possibly read any significant portion of these memos. They mostly just maintain the system which puts them in a database which is searchable by many law enforcement agencies. The overwhelming majority are write-once read-never.

Banks are extremely aware that most SARs are low signal, and that a good customer might wander into getting one filed on them. But there are thresholds and risk tolerance levels. And SARs will sometimes, fairly mechanically, cause banks to decide that they probably don’t want to be holding a hot potato. It’s risky, plausibly, and expensive, certainly. At many institutions, for retail accounts, the institution will have serious questions about whether it wants to continue working with you on the second SAR. It will probably not spend that much time thinking deeply about the answer.

So can the bank simply explain to the customer that staff time preparing SARs is expensive and that routinely banking customers who turn out to be real money launderers is a great way to end up with billion dollar fines? No, they cannot.

The typical individual named in a SAR is low-sophistication and cannot meaningfully participate in a discussion with a Compliance officer, because they’re very probably at the social margins. Do you have a favorite axis of disadvantage? Immigrant, no financial background, limited English ability, small business owner, socioeconomic class, etc? The axis has non-zero relevance to one’s probability of getting a SAR filed on oneself due to innocent behavior. Very many people who have SARs filed on them are disadvantaged on several axes simultaneously.

No, the bank cannot explain why SARs triggered a debanking, because disclosing the existence of a SAR is illegal. 12 CFR 21.11(k) Yes, it is the law in the United States that a private non-court, in possession of a memo written by a non-intelligence analyst, cannot describe the nature of the non-accusation the memo makes. Nor can it confirm or deny the existence of the memo. This is not a James Bond film. This is not a farce about the security state. This is not a right-wing conspiracy. This is very much the law.

If you work at a regulated financial institution, in the U.S. or any allied country, you will be read into SAR (and broader AML) confidentiality within days of joining. You will be instructed to comply with it, very diligently. If you do not, your employer may suffer consequences. You personally are subject to private sanction by your employer (up to and including termination) and also the potential for criminal prosecution. If your trainer speaks with a British accent, they will phrase the offense as “tipping off.”

It’s not just illegal to disclose a SAR to the customer. It is extremely discouraged, by Compliance, to allow there to be an information flow within the bank itself that would allow most employees who interact directly with customers, like call center reps or their branch banker, to learn the existence of SAR. This is out of the concern that they would provide a customer with a responsive answer to the question “Why are you closing my account?!” And so this is one case where in Seeing like a Bank the institution intentionally blinds itself. Very soon after making the decision to close your account the bank does not know specifically why it chose to close your account.

This strikes many people as Kafkaesque. (Me, too!) It is the long-standing practice of banking in the U.S. and allied countries. It is downstream of laws passed by duly elected representatives. It was not capriciously developed as a political tool in the last few years. (We’ll get to those.)

Crypto-investing VCs are not low-sophistication operators of the corner bodega. They are extremely aware that crypto is on the high-risk list at many institutions. They would prefer this were not so.

Their preferences regarding the high-risk list at, say, portfolio fintech companies are sophisticated and nuanced. For example, they will (accurately!) say that the high-risk list authored by a company socially close to them did not arise in a vacuum. Certain entries were foisted upon them by financial partners. Their financial partners will, over drinks at the bar, very quietly, say that they can relate to occasionally feeling powerless. And, though many will find this dumbfounding, their regulators will frequently say the same thing.

Occasionally. About some entries. We shall return to the mechanisms.

Debankings of founders as opposed to firms

Plausibly some crypto founders are low-sophistication about the finance industry in their early days as founders. This is not a judgement about one's character. Nobody is born knowing everything, and very few people will have a serious and informed encounter with this topic ever, not in school, not at work, not in being a generally well-read individual, unless and until it is professionally relevant to them.

Perhaps a founder might ask a friend: “I run a legitimate business which happens to be in crypto and suddenly found my personal accounts closed. Why did this happen? I did nothing wrong.”

Playing the odds? The bank thinks there is an unacceptable risk that you will use your personal accounts to launder money on behalf of the business (and/or its customers, etc). The bank has insufficient controls to give them an appropriate level of certainty as to whether you’re doing this or not. They are disinclined to find out the hard way, so they invite you to find another bank.

Why do they think you might launder on behalf of the business? In part because of the extensive history of crypto companies laundering funds through the accounts of their founders and employees, specifically, and the banking industry’s highly-evidenced belief that businesses and their owners routinely commingle funds, generally.

Tether maintained access to the banking system by, among other mechanisms, having their executives establish accounts in their own names, stashing funds in the name of a lawyer, and using their non-executive employees as money mules. SBF had many talents but one of the main ones was money laundering. A major mechanism for that was loaning money (mostly customer assets and mostly sham loans) to employees then representing to banks (and others) that the employee was making an independent transaction not affiliated with FTX/Alameda/etc.

One would have to be very new or very incurious to be interested in crypto companies and be unaware of this history. Banks were rarely incorporated yesterday, and certain varieties of incuriosity-with-benefits are extremely frowned upon.

Presumption of innocence by commercial providers

But there is something to the critique, by advocates, that rampant lawlessness within crypto for a decade and a half shouldn’t cause an institution to stereotype an innocent crypto founder. Advocates want banking to follow an investigation uncovering a) strong evidence there exists b) a particular articulable risk which c) society actually cares about.

Part of it is philosophical: they believe they are entitled to something like individualized attention and a presumption of innocence. This assumption is deeply embedded in our legal system.

We do not have this assumption embedded in our banking system.

It would be laughable for credit accounts: “I have never defaulted on a loan from you, and therefore, you must give me the benefit of the doubt, and issue this loan.” No intellectually serious person expects that from banks. No, we construct probabilistic models about who is likely to repay based on observable factors, less some factors which society has disallowed us from using under the law. If we deem you insufficiently likely to repay the loan, even if you are still very likely to repay the loan, you don’t get the loan. Finance is not high school; 92% is not an A- anymore. We don’t have to wait for you to default, or have any individualized suspicion about you, or conduct a years-long fact-finding process.

One is prohibited in discrimination in lending on basis of, for example, race. Why? The American people feel quite strongly that they want this to be true, and so their representatives passed a series of laws. Those laws are well-established and uncontroversial. You also, as young data scientists quickly learn, can’t use customer zip codes, no matter how probative they are. This is because they have a very high risk of being an effective proxy for race. (Aside: this is why California used zip codes when it wanted to prioritize the delivery of lifesaving healthcare to patients of favored races, primarily for political reasons.)

One is not prohibited from using someone’s occupation or ownership of a business as underwriting criteria. Those happen to be incredibly probative and, not incidentally, separate rules literally require that we ask. (AML rules require a bank opening an account with ongoing transaction capability to ask for what your source of funds will be, which will often include wages and/or business income, and banks then generally need to know “... OK, wages for what?”)

Is there a built-out appeals process or higher authority with respect to being declined banking services? Don’t our moral intuitions require there to be one?

Many people with “capitalist” in their job title will tell you that there is, indeed, a higher authority to complain to if a capital allocator rejects your pitch. It is Mr. Market. That capital allocator has competitors. Go pitch them. Are there projects that no capital allocator will fund? Absolutely. That’s an important part of why we pay allocators: they assist us in not frittering away resources society expects to fund e.g. teachers' retirements on non-productive uses.

And so allocators will tell you: If you can’t find any allocator who will back you, despite your belief you have a good business plan, and your business plan requires capital to execute, you do not have a good business plan, and you should do something else with your life.

I have yet to meet a venture capitalist who believes that passing on a pitch should be subject to review by a higher authority than their partnership. Many do not, as routine practice, tell entrepreneurs why they passed. Pure downside. Passing is not an invitation for the founder to work their persuasive magic on you. The meeting was the opportunity for that; the meeting is over.

But banks are, certainly, not venture capitalists. There is an aspect to banks which is not exactly dissimilar in character to infrastructure providers. Utilities are frequently invoked as an example here. Why would we construct a society in which power companies needed to make investment decisions in supplying power?! (I think people surprised there may be surprised to do deep dives into e.g. negotiating power purchase agreements.)

Banks, in addition to providing infrastructure, are also neck deep in capital allocation. Some bits of the bank might be more like one's conception of a power company, and some bits of the bank might be more like one's conception of a venture capitalist. And some bits might be confusing hybrids of two intuitions.

It may surprise you that a simple vanilla deposit account is both infrastructure and also a capital allocation decision.

For one thing, typical deposit accounts in the U.S. are actually credit products. It's baked in and can't be baked out without making them unfit for purpose.

For another:

Banking reputable, legal crypto businesses is a risky endeavor

Sources of credit risk to the bank are substantially broader than simple non-repayment of funds borrowed. A financial institution can take a credit loss on banking a business without having what most non-specialists would consider a credit relationship. This is particularly true when banking financial service providers.

Here’s a worked example:

Suppose a crypto exchange blows up out of nowhere, in an absolutely freak accident that happens in about 20% of all exchange-years. The last financial institution banking them can end up holding the bag.

Voyager Digital was a regulated institution that was publicly traded. It had adults at the helm, a Compliance department, some level of written risk processes, and legitimate backers, including well-known venture capitalists.

Voyager blew up, because none of the above are sufficient to prevent you from blowing up.

When they blew up, their bank (Metropolitan Commercial) received a slew of ACH reversals. Customers (often quite reasonably!) felt that they had sent in money to buy crypto, but they hadn’t received their crypto, which feels quite a bit like fraud, and so they complained to their (the customer’s) bank.

Metropolitan characterizes that complaint as fraudulent behavior. There are certainly fraudulent accusations of fraud made to abuse cryptocurrency exchanges, by paying for crypto, claiming you didn’t get the crypto, and then getting your money back while you keep the crypto. However, the customers Metropolitan wanted permission to stiff perceive themselves as having no money and also no crypto. The customers had traded money for a claim against a bankruptcy estate.

Crypto is a product with widespread adoption across the socioeconomic spectrum, I am told. Do you think a random person off the street would, on being asked "Define a claim against a bankruptcy estate?", have a really confident, automatic answer to that question? I think they would probably have a more confident answer to the question "Have you ever tried to buy a claim against a bankruptcy estate?"

So what happens if one calls one's bank and says “I opened an app on my phone. I tried to buy something. I didn’t get it. Those bastards kept my money.” Very frequently, your bank’s customer service rep will type some brief notes into a web application then hit a button. The customer service rep is trained to sound helpful when this happens. Their skill with that... varies. They make, oh, $15 an hour and are not trained like a district court judge. They will conduct no real investigation nor careful balancing of facts and circumstances. They are likely entirely unaware of notorious bankruptcies in the crypto industry, which are an infintessimally small portion of all complaints that reach their telephone queue. Customer didn’t get something from an Internet merchant? Push the button, read the script to the customer, disconnect, immediately serve next caller.

That button will, some steps later, mechanically cause Metropolitan to transfer back some money to Voyager’s now aggrieved customer, which (importantly) Voyager did not actually have to distribute, because it was in bankruptcy. Whose balance sheet did it come off of, then? Metropolitan’s. Their shareholders had just performed the sacred duty of equity: taking the credit loss so that depositors didn’t have to.

If you are banking a quickly growing financial services firm which has large daily funds flows, and charging small per-transaction fees and/or earning net interest on deposits, the total amount of money at risk (within the chargeback or reversal window) as of time T can be vastly larger than the total revenue charged for services at all times 0 through T inclusive. A handwavy approximation for it: number of days in the relevant chargeback/dispute window times average daily transaction volume times dispute percentage. (This will be in the low to high tens of percent. It depends on many factors, including the sophistication of your customer base, whether well-informed guides to consumer rights in banking go viral within it, and similar.)

And thus banks are very selective with respect to what financial services firms they bank. Because one blowing up, just one, can sink the entire related business line.

Voyager and Metropolitan ended up asking the court to change the rules of the ACH protocol in their favor. Then banking technologists told the court that the ACH protocol was computer code maintained in a decentralized fashion and thus beyond the purview of any court. Wait, no, that sentence is from my unpublished cyberpunk novel and somehow made it into this essay by accident; please disregard. No serious person would say courts cannot interact with software or the people who write it. The court ordered a protocol upgrade. The court’s order was swiftly carried out, like many court orders, by responsible professionals employed by several firms.

Metropolitan, of course, got sued over the whole Voyager fracas. A major aspect of the lawsuit: Voyager intimated to customers that they would be covered by FDIC insurance and so their funds on deposit were safe. Voyager’s CEO has alleged that Metropolitan’s management suggested this selling point. Voyager’s marketing department published objectively false statements regarding FDIC coverage. “[FDIC coverage] means that in the rare event your USD funds are compromised due to the company or our banking partner’s failure, you are guaranteed a full reimbursement (up to $250,000).”

Marketing departments frequently misunderstand fine distinctions here, which is why, at well-operated financial technology firms, Legal does not let marketing write one single word about FDIC insurance without their sign-off. The fateful two words above are “the company”: FDIC insurance does not and has never backstopped the obligations of non-insured clients of the banking system. It only backstops the obligations of insured financial institutions. (Had Metropolitan failed, Voyager’s customers may have had recourse to FDIC insurance, but Metropolitan did not fail.)

And so the FDIC has not paid Voyager’s customers one thin dime, nor will it ever. It has neither obligation nor legal authority to do so.

The FDIC is institutionally very opposed to fraudulently inducing customers to transact via claiming FDIC coverage. The FDIC is a banking regulator, among other things, and we’ll discuss them more in a moment. But they are, first and foremost, in charge of the deposit insurance fund. Crypto’s history of falsely promising that the FDIC will make customers whole for its own failures is one reason why the FDIC is institutionally wary of crypto.

Metropolitan then ceased crypto banking. Several banks which had major or incipient crypto practices ceased crypto banking roughly contemporaneously.

Was Metropolitan within its rights to do so? Ab-so-lutely.

Was it within its power to not exit crypto banking? Some thumbs were placed on the scale, and Metropolitan acknowledges this, though they probably were not dispositive for Metropolitan specifically. Their incipient crypto business blew up in their face. Heads would likely have rolled in any event.

Metropolitan characterized their decision as influenced by commercial and regulatory concerns, but long coming. Quote:

Today’s announcement of our exit from the crypto-currency related asset vertical represents the culmination of a process that began [six years earlier] in 2017, when we decided to pivot away from crypto and not grow the business.

Suppose you are an internal advocate for crypto at a mid-sized bank in the U.S. When you bring your proposals to management, one of the things that will cause a chilly reception is the regulatory environment, certainly. Another one is that management can read the newspaper. Other banks which got this pitch and greenlit it took huge losses, ate months of negative headlines, and will be under examiner’s microscopes for at least the next year. This happened over almost no revenue. Why should management say “Yes, as long as it is only the high-quality crypto companies, as long as you cross your Is and dot your Ts, this seems like a low-risk business to be in? Yeet me some Shiba, bro.”

Anyhow, when a crypto founder couldn’t find a bank in 2011, one could be excused for blaming reflexive banker conservatism and low levels of technical understanding. Crypto has had a decade and a half to develop a track record to be judged on. Crypto is being judged on that track record.

Some advocates consider this unfair. Sure, sure, there was some… cowboy behavior in the early days, but that’s just the price of innovation. The freaks and geeks are always on the cutting edge of technology, and well, you know, I suppose they might not always listen to lawyers. But the early days are basically over. We bring something completely new to the table. We are responsible professionals with a compliance-first mindset. We are thoroughly committed to working with partners in finance and government to assuage all concerns. We have impeccable pedigrees. We say all the right things, in all the right accents. We are capable of hiring lobbyists, making campaign contributions, and engaging in a considered media strategy, too!

Some chill felt is caused by the long shadow of SBF

Much has been written about Sam Bankman-Fried and his co-conspirators and enablers. That story remains extensively misunderstood and undercovered relative to its importance.

SBF et al orchestrated a sequential privilege escalation attack on the system that is the United States of America, via consummate skill at understanding how power works, really works, in the United States. They rooted trusted institutions and used each additional domino’s weight against the next. A full recounting of the political strategy alone could easily fill a book. The forfeiture allegations fill 26 printed pages at 1-2 lines per targeted politician. The United States has also alleged that he tried to buy the Bahamas.

SBF and most of the co-conspirators were focused on the Democratic side of the aisle. His cutout Ryan Salame was the bagman for the Republican side of the aisle. Salame’s own lawyers, in their sentencing memo (pg 11), in what is a unique legal strategy, disclaimed any good intent: “Whatever the topic, Ryan’s ultimate purpose for [meetings with government officials including including Senator Mitch McConnell and then-Congressman Kevin McCarthy, focused on pandemic preparedness] was eventually to influence cryptocurrency policy.”

SBF was not charged for the bribing officials part of the crime tapestry, putatively due to treaty commitments to the Bahamas. C.f. the extradition treaty, Article 3. (I absolutely believe that that was a complication and disbelieve it was a hard constraint.) It was an element of plea deals by several co-conspirators, most of whom got lesser sentences for cooperating with the government. Salame was uncooperative and sentenced to 90 months. SBF’s parents appear unlikely to be charged. This is despite them being active and knowing participants in crime, including providing their son with extensive advice, in writing, on topics germane to their professional expertise. For example, his mother, a Stanford law professor and Democratic bundler, advised him to use his coworkers as straw donors to avoid compromising optics via mandatory disclosure laws. IANAStanfordLawProfessor, but that is plainly illegal.

SBF was considered, for a time, the heir apparent to George Soros. He was the next generation’s well-monied Democratic standard bearer in Washington. One major reason why crypto has experienced what feels like performative outrage from Democrats since 2022 is that they are trying to demonstrate that crypto did not successfully buy them.

Many in Washington, like many in crypto, have… selective memories of what meetings they took, transactions they entered, calls they made, and cookies they noshed on in 2020 and 2021.

But to remove the beam in my own eye before casting out the mote in another’s: SBF struck me as whip-smart, extremely cynical, but sincere with respect to his motivations. I thought him likely one of the most competent operators in crypto. (Don’t assume that I meant that as high praise, please.) Also I understood him contemporaneously to be Tether’s bagman and told people, privately, “Don’t get too close; 5% chance he goes to prison.”

In hindsight, I overrated the competence in several important domains, and totally missed the massive fraud. This was in no small part because of a strong sense of fellow-feeling. We have blind spots the size of Jupiter for people who remind us of ourselves and our closest friends. It’s hardwired into humanity, I think.

Anyhow, Tether’s current most important bagman is Howard Lutnik, who may be stepping back from the position, as he’s currently leading Trump’s transition team and has his eyes on bigger prizes. Forget MicroStrategy’s high implied volatility. Lutnik convertible arb would be the trade of the century.

Some crypto advocates believe it’s unfair to tar the industry with the SBF brush, for either industry internal reasons (“He was CeFi not true DeFi, and tried to force the rest of us along with it! Nuts to him!”) or political reasons (“Not my side of the aisle! Salami, you said? Never heard of him neither!”)

Here we are again at the tension between a) democracies should practice careful consideration of individuals on their merits and reject collective punishment but b) the political system shouldn’t have the memory span of a squirrel.

Operation Choke Point

Once upon a time there was an impressively unprincipled set of decisions made. Like many such tales, it didn’t happen as one discrete event in a smoky backroom. It started small and then cascaded, was covered up, and then came to light. Then, it was roundly and justly castigated.

There are certain incredibly non-salubrious businesses that make routine, intense use of banking rails and which simultaneously generate many customer complaints. Debt collectors are one such business.

Full disclosure: I was an unpaid advocate for consumers with issues with debt collectors (and banks, FWIW) for many years, and have described debt collectors as “among the most odious hives of scum and villainy as exist in the United States.” I’m also grouping a few clusters of consumer credit bottom feeders under “debt collector” or we’d be here all day: payday lenders, so-called “credit repair” companies, and debt-adjacent telemarketing.

Banking regulators, in response to customer complaints (which savvy customers, such as customers who listen to advocates like yours truly, will sometimes route through regulators because that achieves better outcomes than routing through CS), warned banks that debt collectors appeared to be at grossly disproportionate risk of ACH transfers that customers claimed were unauthorized. Customers claiming this are not always being candid. However, debt collectors do routinely abuse one’s common intuitions about how banking rails work as an intentional strategy. See the above piece for elaboration at length.

Now, banks who bank debt collectors can math out how many of their ACH payments are complained about. One can make an argument that those banks might not have institutional knowledge that complaints about debt collectors are structurally anomalously high, for Seeing like a Bank reasons. One could further argue that a regulator can licitly tell a bank something they don’t know. That sounds reasonable and an appropriate use of a public servant’s time.

Those banks that would open accounts for debt collectors (n.b. not all banks!) are OK with having that business. Debt collection, while not salubrious, is legal and regulated in the United States. Banks are not one-stop monitoring shops for all of their customers’ various obligations under the law.

But working through legislatures and courts is slow and expensive. Why not simply deputize the banks? We already have them run private intelligence agencies! How much of a reach is it for them to also run private consumer protection bureaus?

The Obama administration didn’t like debt collectors, for very similar reasons to why I don’t like debt collectors. And so they broadened the critique: the risk in banking bad guys was broader than the (known, accepted, controlled, and certainly not existential) risk of ACH reversals. Those customer complaints, those complaints could harm the bank’s standing in the community. That could result in e.g. a withdrawal of customer deposits. This would imperil the bank, for the usual reason. And if something could imperil banks, why, that should naturally cause the FDIC to make its opinions known.

Get out of peril, by kicking debt collectors to the curb.

But the FDIC had to be persuaded into that point of view, by a cadre of very talented people.

The Department of Justice had a legal theory, which it was quite proud of. The Financial Institutions Reform, Recovery, and Enforcement Act of 1989 (FIRREA) gives the DOJ a hunting license for any fraud (and many other crimes) which affects a federally insured financial institution. FIRREA was passed after the savings and loan crisis, to protect small financial institutions from peril and thereby avoid another crisis.

Now your common sense understanding might be “Oh, Congress probably intended on cracking down on fraud targeting banks which, I don’t know, was big enough to imperil a small community institution? I could see a really large fraudulent bank loan imperiling a small bank. And checking the history books, there were some wildly fraudulent bank loans mixed up in the S&L crisis. OK, so we federalized prosecution of defrauding a bank like that? Sounds reasonable.”

If you have that intuition, you are apparently not creative enough to have worked as a lawyer in the Obama admin DOJ. No, their thought was that if you provide rails which facilitate fraud, such as giving a fraudster a bank account, you are affecting a financial institution: yourself. And so, the DOJ can go after you, for self-harm. Note that you do not need to lose money, oh no, the DOJ can also go after you because the way you affected yourself was to cause your regulator to like you less. When you settle with the DOJ, it will extract an enforceable promise in writing that you will stop your campaign of self-harm, and also stop banking specifically enumerated industries, like payday loans.

I realize that this sounds unlikely. The following is a direct quote (expanding acronyms) from the DOJ Office of Professional Responsibility, in the report (pg 16) where they exonerated DOJ lawyers.

As more fully explained below, the [Consumer Protection Branch] has relied on the “self-affecting” theory, as well as additional theories of liability, in three cases arising from the Operation Choke Point initiative.

Now when the DOJ or FDIC tells you, a bank, to do something, or strongly suggests that you do something, that usually isn’t the end of the argument. You can certainly haggle. You can even fight… to a degree.

This is a multi-year iterated game with repeat players, each of whom has limited resources and very complicated preferences. Both sides are constantly picking their battles. There is give and take. When your counterparty is happy with you, your emails get returned faster, you get more of your asks, and you can report smooth sailing to your boss. Both banks and regulators are ultimately made up of people, with emotions, career paths, and annual performance reviews.

Banks do not actually make a lot of money from servicing debt collectors. The culture that is banking looks at the culture that is debt collection and sees slimy people who are beneath it. And so the banks frequently obliged. Many of them, in their offboarding letters to debt collectors, were unusually candid relative to the standards of offboarding letters: it’s not you, and we apologize for this, but we’ve received regulatory guidance about your industry, and as a result our appetite to serve your industry no longer exists.

As it turns out, the Obama administration had many diverse policy preferences.

It wasn’t particularly in favor of guns, for example.

Gun sellers don’t use banks in the way that debt collectors use banks. They do not routinely trick customers into the gun-for-money transaction. They don’t make particularly intense use of ACH pulls (confidence: 99%, on general industry knowledge) and don’t have particularly high dispute rates (confidence: 95%, same).

But regulators, having discovered that “reputational risk” attached to anyone you didn’t like with nary a whisper of complaint, believed that banking gun sellers was high-risk. Haven’t you read the newspapers? School shootings. Do you want any of that sticking to you? You are imperiling your good name, and therefore the stability of your deposit base, and therefore your bank, and therefore the insurance fund, by accepting the business of gun sellers.

In Congressional testimony, the FDIC said that it hadn’t ordered anyone to debank disfavored businesses.

What we have done is we have tried to be very clear in putting out our guidance to say very publicly and clearly that as long as banks have appropriate risk mitigation measures in place, we are not going to prohibit or discourage them from doing business with anyone with whom they want to do business.

One may be surprised that this individual might perceive themselves as telling the truth here. Because “Justify to me why the payday lenders are not on your high-risk list.” and then “Do you have a built-out EDD program for the deposit risk caused by payday lenders?” followed by “Then are you sure you should accept that business?” are consistent with this statement, individually and as a script. (Those are not quotes, but rather indicative summaries of stages in a conversation. I believe them to fairly characterize conversations that the record abundantly shows happened.)

The FDIC Office of the Inspector General, in an investigatory report, attempted to shift all blame for Operation Choke Point to the DOJ.

We found no evidence that the FDIC used the high-risk list to target financial institutions. However, references to specific merchant types in the summer 2011 edition of the FDIC’s Supervisory Insights Journal and in supervisory guidance created a perception among some bank executives that we spoke with that the FDIC discouraged institutions from conducting business with those merchants. This perception was most prevalent with respect to payday lenders

When a regulator publishes position papers that it wants you to do something, and reiterates this in individualized supervisory guidance, that tends to create a perception in this author that the communicated policy direction was not YOLOed onto the Internet by a room full of monkeys banging keyboards randomly.

As frequently happens, the individual officials who had instructed banks to debank the targeted industries ignored Stringer Bell’s dictum on taking notes on a criminal conspiracy. Emails sent within the FDIC and DOJ were routinely archived, and banks (of course) keep copies of correspondence from their regulators. Those emails said what they said, and what they said was pretty damning.

For example, the Department of Justice’s internal Six Month Status Report On Operation Choke Point (excerpted in Congressional reporting) said:

Finding substantial questions concerning the legality of the Internet payday lending business models and the loans underlying debits to consumers’ bank accounts, many banks have decided to stop processing transactions in support of Internet payday lenders. We consider this to be a significant accomplishment and positive change for consumers . . . Although we recognize the possibility that banks may have therefore decided to stop doing business with legitimate lenders, we do not believe that such decisions should alter our investigative plans.

Not once, not twice, not a handful of times, not a loose confederation of rogue examiners. Three of six regional directors of the FDIC offices told the OIG that they understood Washington to want payday lending discouraged and two of them said there was an expectation to, in the words of the OIG, direct institutions that facilitated payday lending to “pursue an exit strategy.”

Did that require top-down direction? You can, in fact, generate nationwide programs with local offices doing strikingly similar things without top-down direction. The combination of a monoculture plus a policy direction that lower-level staffers believe in is often sufficient to make it happen. We have extensive experience of this in tech and finance, as discussed later.

Japanese has a beautiful world, sontaku, for the attitude and actions a diligent subordinate would take without his superior’s explicit instruction, believing them to anticipate his boss’ desires. Sontaku is a core skill in the American professional class. People possessing it are sometimes described as “motivated self-starters”, “high-agency”, “bold”, ”takes initiative”, ”acts like an owner”, etc. You are a very, very bad Compliance professional if you aren’t constantly sontaku-ing your regulator. You are also a bad Regional Director of the FDIC if you aren’t constantly sontaku-ing Washington.

But Operation Choke Point, specifically, simply was official policy. If it wasn't, no entity as complicated as the United States can ever be described as having even once had an official policy.

As the former Chairman of the FDIC wrote in a WSJ editorial:

Internal Justice Department papers released by the House Oversight and Government Reform Committee make it clear that Justice prefers coercing banks to drop customers through Operation Choke Point rather than prosecuting illegal or fraudulent businesses directly because it’s easier, faster and requires fewer resources.

Operation Choke Point wasn’t just targeting debt collectors, gun sellers, and payday lenders. No, the FDIC’s bullet-pointed list was 30 entries long. They range from clearly abusive and illegal (scams) to “One could construct a narrative by which banking that industry is challenging” (pornography) to “a grab bag of things we dislike” (racism and… fireworks? Really?)

Operation Choke Point, once it came to light, caused a media and Congressional furor, because it was arbitrary and lawless. (I am using that in the ordinary sense of an American who took civics, not in the specialized sense of a DOJ lawyer, who might bristle for being called “lawless” when they had three court cases and one 25 year old statute which are clearly explained in the memo as adding up to them being able to do everything they did.)

The architects of Operation Choke Point steadfastly denied it was designed to do what it was manifestly designed to do. They denied it did what it manifestly did.

The agencies were then pointedly accused of lack of candor with Congress. If you tell a Congressman he isn’t reading the WSJ right, but internally your bosses are high-fiving themselves over WSJ article, and they are high-fiving themselves because finally the WSJ is covering their important work accurately, Congress will not be pleased. Then they will show you a copy of your bosses’ emails, which they can subpoena, because they are Congress. (House Oversight Committee report, ibid, pg 10)

Some scholarly literature is sympathetic to the regulators’ point of view. (More is not is not.)

If you want a steelman, that’s the best one you’ll likely find. It acknowledges the DOJ’s efforts to interdict fraud by creatively interpreting FIRREA and targeting third-party payment processors and banks, accuses the financial industry of making a fuss over this for self-interested commercial reasons, performs a modified limited hangout of the high-risk list, and claims that the gun industry cynically glommed onto the news cycle for political reasons despite no actual enforcement specifically addressed against it.

My point of view? I can read emails. They say what they say, even when acknowledging what they say would cost a public servant their job. I read the postmortems (including many years ago; this sort of thing was my hobby before it was my job). I view them as face-saving exercises written, in no small part, by civil servants mortified that their peers could lose jobs and pensions simply for implementing the Administration’s policy preferences using colorable authority.

Sometimes, people have been known to lie in politics. Sometimes justice is not done. I know, try to weather the shock you must feel.

Operation Choke Point was mostly forgotten, except by banking nerds.

Until…

So-called Choke Point 2.0

Nic Carter, a crypto VC and podcaster, who occasionally does very good work, has been steadfastly attempting to brand a constellation of regulatory activities regarding crypto as Choke Point 2.0. This branding is an attempt to delegitimize them by associating them with politically-motivated lawlessness. It has since become popular among crypto advocates.

Unlike Operation Choke Point, which actually was a centrally directed operation with written project plans, status meetings, ongoing progress reports, and a code name decided by the participants (who, in hindsight, should have talked to their own Comms department and picked something that didn’t sound nefarious to describe their plans), Choke Point 2.0 stretches like taffy to attach to any recent regulatory activity crypto advocates don’t like. So we’ll have to review quite an involved history of very disparate issues to give advocates a fair hearing.

Carters' work, which is extensive on this topic, exists in pieces like Did the government start a global financial crisis to destroy crypto?

To answer the question in the title: no, it did not. We started a financial crisis which to-date is mercifully narrow as an underappreciated side effect of interest rate hikes to tame inflation.

Silvergate: Crypto had a bank, doesn’t now, and misses the good days

Crypto advocates have specific and general concerns about banking supervision at a small cadre of banks acutely relevant to their interests. They have tied these concerns to the debanking narrative.

They do not evince attention to detail or familiarity with the procedural history of specific examples they invoke, though some have attempted some original reporting with respect to these issues. That is to their credit.

As we’ve established, almost all banks consider crypto businesses to be high-risk, and avoid them. There was a small cadre of banks which had active crypto practices. Those banks purported, to the public and their regulators, to have the EDD required to bank them compliantly. This was incredibly operationally useful for crypto, for one very obvious reason (substantially every business needs a bank account) and one less obvious one.

Crypto talks a great game about decentralization, but centralized systems are more efficient than decentralized systems. When riding banking rails, making transfers outside of regular banking hours (which have five twos of uptime) is difficult. This exposes firms to risk and acts as a constant cost of capital.

Crypto trades 24/7. Crypto firms would like to settle crypto trades, particularly between stablecoins and the USD backing them, 24/7. Crypto’s solution to this was to all bank at the same bank, Silvergate, which I described (with some surprise, when they IPOed) as the First National Bank of Crypto.

Silvergate had a particular product called the Silvergate Exchange Network (SEN). SEN was both a) boring infrastructural plumbing and b) extremely important to the crypto industry. Oh boy, do crypto companies miss SEN. In sum, SEN would allow substantially 24/7 book transfers between Silvergate customers to shift USD balances between their bank accounts. This would let them constantly settle the USD leg of crypto trades between each other.

This was particularly important for stablecoin issuers, like Circle, which issues USDC. Circle’s main custodial bank for USDC was SVB. Circle wanted to be able to issue marketmakers like DRW and Alameda Research hundreds of millions of USDC 24/7 at any hour on any day with no more than a few minutes of latency, or redeem USDC for greenbacks in a similar fashion.

Now, a thing you will frequently see in fintech banking, and which is not itself at all inappropriate, is a fintech having multiple banks with a division of labor. One of those banks might agree to have a fintech’s customer-facing high-velocity low-EOD-balance transactional activity. And one of those banks might agree to have a fintech’s low-velocity high-EOD-balance deposits. These are very different business propositions for the banks! They imply different risks, different core competencies, and different revenue opportunities.

If you are running businesses which both a) have high daily inflows and outflows and also b) want to keep billions of dollars in the regulated banking perimeter, you very much need partners comfortable with both halves.

The argument you make, as a fintech, to the bank with your deposit business is that the other bank is also a competent, U.S.-regulated financial institution, with good AML and KYC controls (among others). Therefore, when your business makes one wire at the end of the day to settle up with its omnibus account at that bank, netting over several hundred thousand customer transactions, perhaps for several hundred million dollars, your bank should be comfortable, even if it has very little exact knowledge about what happened today.

Probably the same story as yesterday, and tomorrow, and Compliance can sleep the sleep of the righteous, because their trusted peers have an appropriate degree of controls in place. The bank custodying the money mountain is thus certainly not aiding and abetting money laundering. It can rely on the second bank’s own surveillance and controls, in addition to the crypto firm’s compliance department. There will be many formal contractual promises and informal verbal or written assurances made about this. And this works and serious people can accept it but the factual probity of the high-velocity transactional bank is extremely load-bearing.

Silverbank was not a competently run institution.

SEN did not, in fact, have a robust controls environment. It, in fact (para 70), had functionally no transaction monitoring. Silvergate had bought a standard package that a lot of banks use for automated monitoring, but due a configuration issue, it was off for SEN transactions.

Carter describes this state of affairs as follows: “Silvergate’s transaction monitoring system for SEN had gone through an upgrade and experienced an outage.”

Silvergate was institutionally aware of the “outage” but unable to remediate it.

I have an engineering degree, have founded five software companies, have worked in the tech industry, and in my entire career, I have never described an engineering investment I failed to make for fifteen months as an “outage.” After a day it is an outage, after a week it’s a human competence issue, but after a year it ferments into sparkling tech strategy.

During that period, SEN transacted over a trillion dollars. Silvergate was not unaware that SEN had an up-and-to-the-right usage graph (congratulations!). They were just routinely ignorant of funds flows they were facilitating with their banking license, sized in the billions of dollars per day. We know this because of Silvergate’s contemporaneous internal communications, the technical reality of the artifacts they had purchased and implemented, and sworn statements in litigation and to regulators. It is beyond intellectually serious dispute.

What of it, though? Is that just a harmless paperwork glitch? I'm glad you asked.

Intrabank book transfers are historically low-risk for money laundering because they’re ineffective at accomplishing layering: the same Compliance department can see both legs. Moreover, the majority of them are between entities known to be under common control. The purpose of layering is to break the chain of surveillance; swapping between your left pocket and your right pocket in front of a Compliance officer doesn’t accomplish this. This assumption of low-risk was apparently, per Silvergate’s employees, baked very hard into ATMS-B, the new-and-improved monitoring suite Silvergate had implemented.

However, SEN transactions, while implemented as intrabank book transfers, are in fact high-risk. The designed intent of SEN is to allow counterparties not under common control to settle one half of a transaction, at very high velocity. The other half generally occurs on a blockchain, unsurveilled by the bank. If you can’t see that half, and you can’t see your half, why, that sounds like you are swapping bank deposits for cash equivalents sized in the billions of dollars per day with no functional AML monitoring program in place.

This is not just me saying it. Kathleen Fischer, Chief Risk Office of Silvergate, said internally, of the lack of SEN monitoring: “We have known of this issue and either we have established other controls to account for it or we haven’t, and we have to take our lumps.”

Silvergate had not, in fact, established other controls.

Carter claims that all clients of the bank had gone through rigorous KYC and onboarding processes. Silvergate may have consistently conducted KYC and onboarding processes, but one could forgive a skeptic for believing them to be pro forma.

Silvergate onboarded several entities relating to Binance, a confessed criminal conspiracy which extensively engaged in money laundering. Binance and its management are Bond villains; they gleefully flouted the law and engaged in jurisdictional gamesmanship to avoid financial regulation, for years. Binance et al transacted $22 billion through Silvergate.

Mandatory compliance training is such a drag, and sometimes we like to spice it up with fun games. Let's play Spot the Red Flags together.

We have just received an account application from a Seychelles-docimiled corporation beneficially owned by a globally notorious billionaire. He disclaims any permanent address. The beneficial owner receives regular negative news coverage. He and his company have received multiple orders to cease business from peer nations. Those orders cite offering financial services without a license, suspicion of money laundering, willfully non-compliant posture, and extensive documented lies to regulators. The corporation has no operations or employees; it is strictly a shell. The planned funds flow is receiving inbound wire transfers, including international wire transfers, from counterparties which the bank will have only fragmentary third degree knowledge of. The corporation intends to immediately transfer those deposits to a third-party financial institution. This is to facilitate those counterparties’ purchase of pseudonymous bearer instruments, specifically, cash equivalents. The corporation anticipates billions of dollars of volume, in transaction sizes up to eight figures.

Silvergate happily opened an account (pg 4) for Key Vision Development Limited, the above-described shell company, and allowed it to deposit and withdraw over $11 billion. Now, credit where credit is due, Silvergate did debank Key Vision Development Limited in 2021. The record doesn’t say why, but perceptive readers may be able to hazard a guess. But Binance’s main entities still enjoyed attentive service, or perhaps more to the point they enjoyed all the inattention they were getting with their service, until the bank folded.

But the main rake Silvergate stepped on, repeatedly, was its relationship with FTX/Alameda and its executives. They were collectively the bank’s largest client and comprised tens of percent of its deposits. Silvergate’s monitoring of their usage was minimally grossly inadequate, as the bank and its executives admit.

Carter quotes an unnamed Silvergate executive as saying the following, which is roughly consistent with their prior statements to the media and to regulators.

Where we were not as buttoned up as we should have been was in regards to the FTX/Alameda clients. That was a function of the bank growing incredibly quickly[.] … Probably we could have figured out FTX was brokering deposits via Alameda. In retrospect I think we could have pieced this together and figured it out. But this is not a legal failure and we’re not required to catch everything. Our program passed legal muster. That’s something we could have done a better job of. But there was no intentional wrongdoing or cooperation with the bad guys.

This is consistent with things they have said previously, but does not demand unlimited deference.

Ryan Salame, a subject matter expert in laundering crypto money through the banking system (skills described by his lawyers, see pg 7 and onwards), tweeted that it beggars belief that Silvergate did not know that Alameda Research and North Dimension were in fact receiving FTX customer funds flow. Salame has repeatedly stated that Silvergate intentionally orchestrated that funds flow in concert with him. Even if it had not, Salame is just right: even if FTX concocted the scheme internally and even if Salame somehow managed to push all the buttons himself, Silvergate had to know.

But suppose you credit neither Salame nor I with understanding how banks work, or you demand unquestioning deference to executives’ denials, perhaps because one believes that a bank executive would never ever lie. The picture most favorable to Silvergate is that, during multiple years of being monomaniacally focused on growth to the neglect of its responsibilities under the law, it routinely underperformed the competence bar required of regulated financial institutions in the United States.

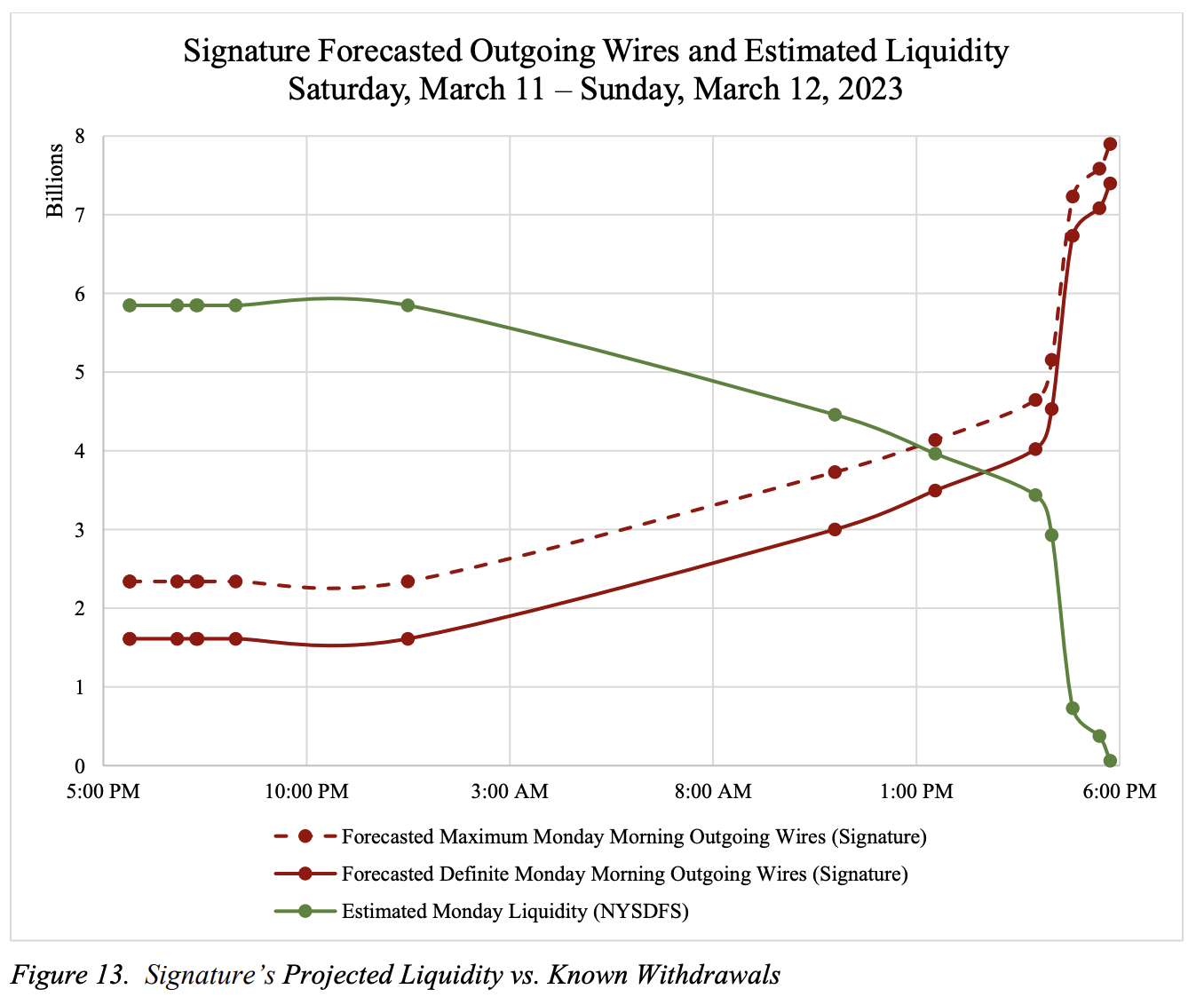

Silvergate voluntarily liquidated in the wake of the FTX implosion. Limited props for them here: they managed to do this in a mostly orderly fashion, as opposed to Signature, which had substantially less crypto exposure but blew up. (Signature had an analogous book transfer API product, called Signet. It is a smaller part of their story.)

Carter has a number of complaints with regards to supervisory activities relating to Silvergate Bank. One of those is that he alleges the Office of the Comptroller of the Currency disallowed Silvergate from selling SEN. I find this allegation very plausible, if not specifically evidenced. Silvergate was operating a trillion dollar laundering machine which had drawn immediate demands for corrective action for an extended period, had not taken aggressive corrective action, and then had proximately caused enormous consumer harm in a way which was maximally embarrassing to many policy actors. When the bank’s Chief Risk Officer predicted incoming lumps, these were the sort of lumps she was predicting.

Carter further alleges, and I think this is substantially original reporting (and good on him for it), that the FDIC and other banking regulators gave verbal guidance that banks should get crypto deposits below 15% to be “safe and sound.” If a banking regulator invokes those words, they are not making a suggestion. Carter complains that there is no statutory authority to pick this arbitrary number, that this threshold makes banking crypto functionally impossible, and that it is specifically chosen to kill targeted banks.

Some regulators are disclosure regulators. The SEC comes to mind. Some regulators are prudential regulators. The ordinary operation of prudential regulators is to take broad statutory direction and transform it, sometimes via the rulemaking process and sometimes via more informal guidance (and, even the FDIC will tell you, “moral suasion”). This process yields both concrete asks and fuzzier spectral ranges subject to ongoing negotiation between regulators and the regulated.

Does the FDIC have statutory authority to pick magic numbers? Yes, in the political system of the United States, it does, and it can cite that authority to you at length. The FAA has statutory authority to pick magic numbers for bolt torque. The FDA has statutory authority to pick magic numbers for permissible flow rates for ketchup.

Are regulators overreaching here? Not obviously so! Look at the above description of Operation Choke Point and their theory of regulatory authority there. It requires magical thinking to connect banking a payday lender, reputational risk, a run on your bank, and endangering the deposit insurance fund. It very much does not require magical thinking to think that crypto deposits are flighty, correlated, and could cause a run! We were experiencing actual crypto-induced runs!

A reasonable argument can be made that the problem with regulators was not abuse of discretion. It was needing to pay for past regulatory mistakes and/or missed opportunities with overcorrection following substantial consumer harm. Examiners (stunningly) missed that Silvergate’s new business model, which they had IPOed on the strength of, had materially changed from its days as a sleepy two-branch real estate bank! That reasonable argument has been alluded to… by the Federal Reserve! See Findings, pg 2.

Does the 15% threshold make it generally impossible to bank crypto? Empirically not; other bank’s crypto practices are well beneath that threshold, which likely informed how it was chosen. Metropolitan, for example, had about 25% at the peak and then drew down to 6%. It fairly persuasively told stakeholders that it had done a good job of risk management. And, not incidentally, Metropolitan is still with us. And so regulators could very reasonably say: “OK! 6% is all-else-equal green, 14% is yellow, we don’t want you spiking to 25% anymore, 96% is deep #%*(#(ing don’t even think about it red.”

And you could make this same observation about many banks with a crypto practice. Coinbase doesn’t keep customer’s money in a mattress. Their main bank’s crypto exposure is… <Jamie Dimon grabs the keyboard>FORTRESS BALANCE SHEET</Dimon not actually grabbing the keyboard>.

Carter further alleges or insinuates (it’s a bit unclear at times which he is going for) that Senator Warren and/or regulators colluded with short sellers to intentionally kill Silvergate, via sparking a liquidity crisis.

He specifically cites a this letter by Warren et al, which includes the sentence “Should it need extra liquidity, your bank has access to taxpayer dollars through the Federal Reserve Bank of San Francisco and the Federal Home Loan Bank of San Francisco.”.